Tata Motors DVR Share Price: A Dual-Class Investment Opportunity

2023-07-26

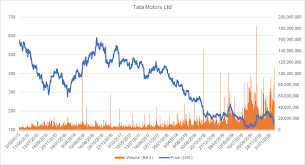

Unveiling the Dual-Class Structure: Understanding Tata Motors DVR Shares Tata Motors, a well-known automotive company, offers an unusual investment option with its Dual-Class Structure, which includes both ordinary shares and Differential Voting Rights (DVR) shares. Understanding the drivers underlying Tata Motors DVR share price becomes critical as investors seek diversityContinue Reading